The Yen: A Comeback Story

For decades, the Japanese yen has occupied a quasi-sacrosanct position in global FX markets. Structural current account surpluses, chronically low interest rates, and macroeconomic stability rendered the yen a textbook funding currency and episodic “safe haven.”

The post-2021 episode was different. The Fed-led global tightening cycle collided with Japan’s off-path easing, producing one of the sharpest yen depreciations in modern history. That move was internally consistent: widening nominal rate differentials, unhedged capital outflows, and FX pass-through into import prices reinforced one another.

What no longer makes sense is what followed. As advanced economies now pivot toward easing, and Japan is the only major economy still normalizing policy, the yen has continued to weaken. From a first-order macro and rates framework, this is incoherent. The explanation lies not in fundamentals deteriorating—but in markets failing to internalize a structural regime shift in Japanese inflation, policy reaction functions, and FX transmission.

Core Thesis 1: A Regime Shift in Japanese Inflation and the Case for Sustained Normalization amidst a decreasing US/Japan rate differential environment

Japan’s inflation dynamics have shifted decisively after more than two decades of deflation, with inflation now durable rather than transitory as price pressures have broadened from imported energy and FX pass-through into core and services. Tokyo core CPI rose 2.8% y/y in November 2025, and inflation has stayed above the BOJ’s 2% target since March 2022. Critically, inflation is now being validated by wages, with the strongest Shuntō outcome in over 30 years (5.25%) alongside persistently low unemployment (2.6%), indicating a transition from episodic inflation to a self-reinforcing wage–price dynamic, reinforced by expectations that 2026 wage settlement increases will persist.

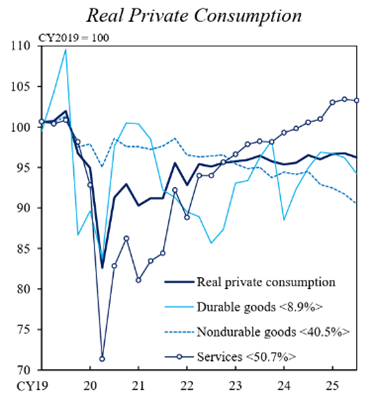

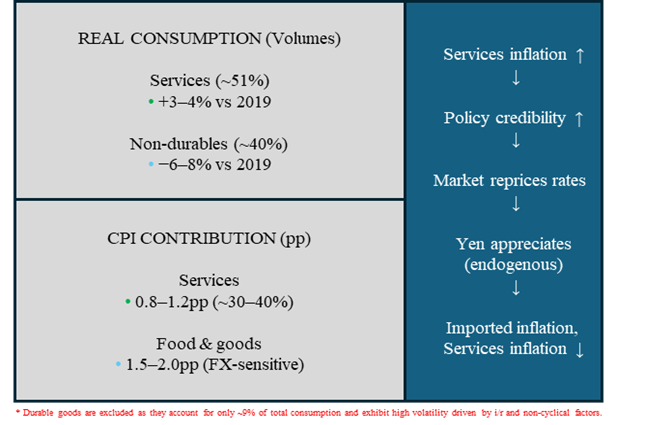

A granular decomposition of consumption and CPI shows that post-2022 inflation in Japan is bifurcated. Inflation in non-durable goods—around 40% of private consumption—has been predominantly cost-push, with prices rising even as real non-durable volumes remain ~8-9% below their 2019 level, consistent with import-cost and FX pass-through. By contrast, services—accounting for ~51% of total consumption—have experienced a sustained real activity overshoot of ~3–4% above pre-COVID levels by 2024–25, and now contribute roughly 0.8–1.2 percentage points, or ~30–40%, of core CPI inflation. This represents a significant departure from Japan’s historical inflation episodes and points to a potential regime change.

The distinction is policy-relevant: non-durable inflation (food and goods) is highly sensitive to the exchange rate, reflecting Japan’s import dependence, with approximately 60% of caloric intake imported, whereas services inflation—driven by labor-market tightness and largely insulated from FX— responds primarily to policy rate adjustments. The emergence of demand-driven services inflation therefore raises the likelihood that monetary tightening will be sustained, in turn increasing the probability that markets support yen appreciation. Essentially, two birds can be killed with one stone.

Source: BOJ

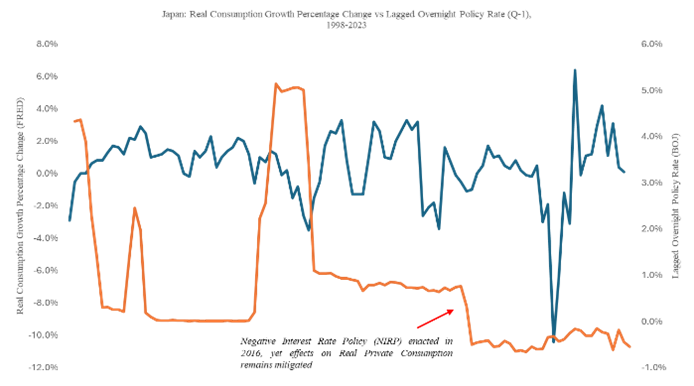

Despite this, Japan’s real policy rate remains deeply negative, keeping monetary conditions accommodative despite recent tightening. In December 2025, the Bank of Japan raised its policy rate to 0.75% (from 0.50%), the highest since the mid-1990s, yet meeting minutes explicitly note that rates remain “too low relative to inflation.”

Crucially, Japan’s normalization is unfolding as the U.S. policy path shifts in the opposite direction. Market pricing—visible in the concavity of front-end yield—alongside guidance in the December Federal Reserve minutes increasingly points to rate cuts in 2026, supported by cooling labor markets and a downtrend in core inflation.

Core Thesis 2: Fiscal Constraints Conducive to Sustained Monetary Adjustment and Yen Appreciation

In principle, inflation can be addressed through either fiscal consolidation or monetary tightening. In Japan, however, fiscal adjustment is politically constrained, shifting the burden of stabilization decisively onto monetary policy and the exchange rate. The approval of a record ¥122.3 trillion FY2026 budget, alongside a ¥21.3 trillion stimulus package announced in late November 2025—the largest since COVID—confirms the government’s continued reliance on fiscal support. This bias is reinforced by Prime Minister Sanae Takaichi, the most fiscally expansionary candidate to emerge from the LDP leadership contest.

By contrast, Japan’s economic structure—characterized by high domestic cash allocation and low household leverage—implies a substantially lower elasticity of private consumption w.r.t policy rates than in other advanced economies. Given that private consumption accounts for roughly 60% of GDP, this muted responsiveness dampens the contractionary impact of monetary tightening on aggregate demand. As a result, monetary tightening emerges as the least politically costly solution, allowing policymakers greater scope to raise rates without triggering a consumption-led slowdown.

Source: BOJ

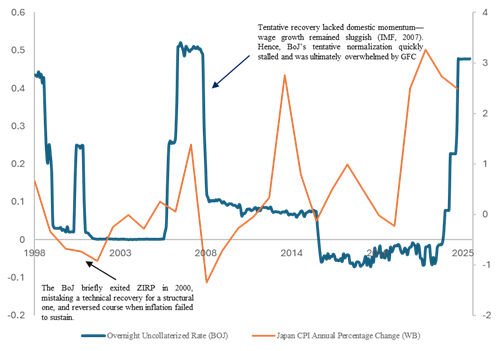

Unlike earlier episodes of episodic and reversible tightening, today’s configuration supports durable policy convergence. The 2000 and 2006–07 “false dawns” were driven by idiosyncratic noise, while the 2014 CPI rise was induced by VAT hikes. By contrast, today’s inflation appears more structural—driven by wages and expectations—making yen appreciation a more credible outcome.

Source: BOJ

Core Thesis 3: Japan’s Overseas Asset Stock Makes Yen Appreciation Operationally Easy

Japan holds the world’s second largest positive net international investment position (¥533.1 trillion end-2024), built up through decades of outward capital flows under ultra-loose policy. During this period, FX hedging was unattractive: when U.S. rates exceeded Japanese rates by several hundred bps, forward hedging erased most foreign yield advantage. Hence, Japanese investors maintained low hedge ratios under the assumption of durable ZIRP/NIRP. This assumption has begun to break down amid a more volatile domestic rate environment (eg. 2024 Nikkei Drawdown).

This configuration creates a low-hanging fruit for FX adjustment. As Japanese rates rise and U.S. rates fall, the hedging penalty compresses. Domestic asset managers do not need to liquidate foreign holdings—risking price impact—or reinvest domestically with uncertain return expectations to generate yen demand. Instead, incremental repatriation can be executed through derivatives, creating latent yen demand that is operationally easy to unlock. This channel materially strengthens policy transmission from monetary tightening to yen appreciation.

Supporting conditions reinforce this mechanism. The Nikkei has reached record highs (up by 80% 5Y). From the rates side, the BOJ has introduced and maintained quantitative tightening since 1Q 2024, mechanically reducing supply, while 10-year JGB yields have risen to ~2.0—levels. Domestic assets are never as attractive as now.

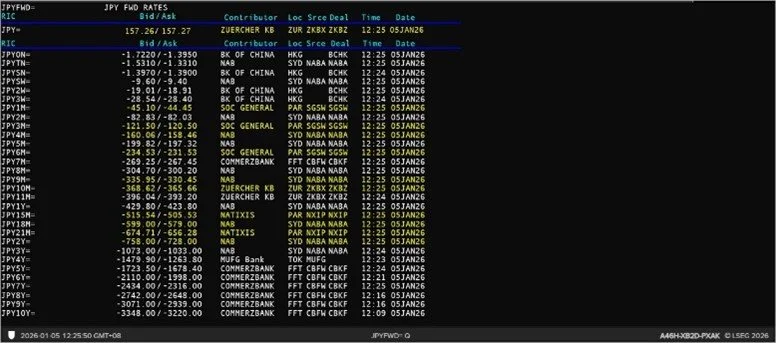

What Is Currently Priced

OTC USD/JPY forward pricing indicates negligible Yen Movement. Sell-side sentiment is bearish as well.

Source: Refinitiv Workspace

However, I expect meaningful yen appreciation over 3–18 months, driven by credible BOJ tightening, rate-differential compression, and large FX hedging flows once carry fades.