India: The Next Manufacturing Hub?

China’s dominance in global manufacturing is largely rooted in its vast population, which provides an abundant supply of low-cost labor. This cheap and plentiful human capital allows fixed costs to be spread over a large output base, significantly reducing per-unit production costs and enabling competitive average selling prices for Chinese-manufactured goods.

From an economic development standpoint, the path to catch-up growth often follows a familiar sequence: beginning with agricultural reform, transitioning into industrial expansion, and eventually culminating in the growth of high-end services. India, with its ambition to emerge as a major global power and counterbalance China’s influence in the Asia-Pacific region, recognizes the pivotal role of industrialization—especially manufacturing—in this journey. Therefore, it has proposed a “Make in India” policy objective in 2014. It has three primary objectives:

1) Increase the manufacturing sector’s growth rate to 12-14% per year

2) Create 100 million additional manufacturing jobs in the economy by 2022

3) Increase manufacturing sector’s share to GDP from 15% in 2014 to 25% by 2022

Has it worked?

While the prevailing consensus holds that the policy has fallen short, this claim warrants verification.

Prima facie, it seems that while growth was present in the manufacturing sector, it was not sufficient. Data analysis of index-level growth in India’s manufacturing sector indicated a halving in CAGR instead from an expected increase since the implementation of the “Make in India” policy. From an absolute perspective, it seems that the policy has not lived up to expectations.

Fig 1. Disappointing growth in India’'s Manufacturing Sector despite government initatives. Source: Ministry of Statistics & Programme Implementation

If we look at gross value-add from manufacturing, the data tells a similar story. However, CAGR in Gross-Value added has experienced a far smaller decline than absolute growth in manufacturing. One possible explanation of this amortizing effect is the transition in manufacturing to higher-margin industries, which increases unit productivity.

Fig 2. Gross-value added Manufacturing share of GDP tells a similar story. Source: LSEG Workspace

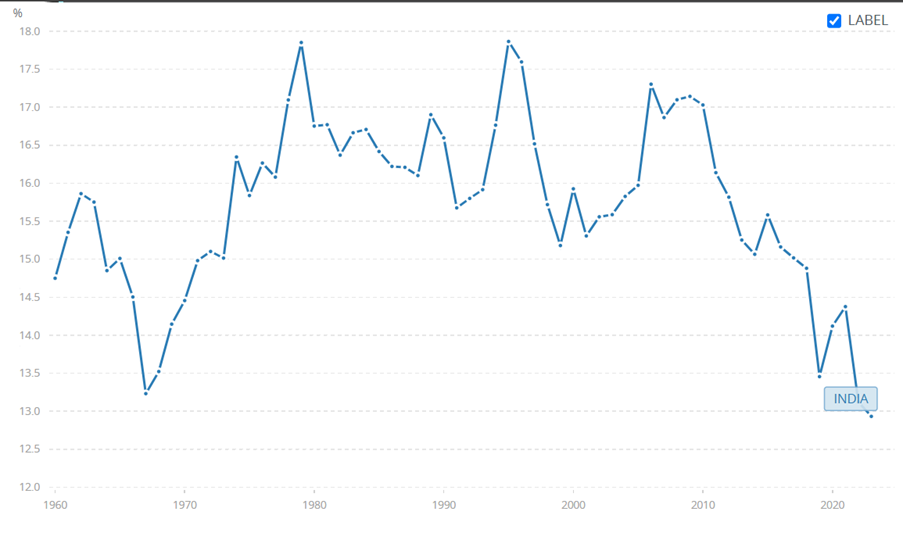

This is evidenced by concrete government strategies aimed at shifting from low-margin textile production to higher-margin industrial processes—particularly in electronics manufacturing, which has grown five-fold since 2014/15. Nonetheless, the decline in the manufacturing industry suggests that per-unit efficiency in output did not compensate for the overall underperformance in output. Manufacturing share of GDP has also decreased, as seen below.

Fig 3. Decreasing importance of Manufacturing in India. Source: World Bank

To evaluate its performance relative to other industries like services, I compared the five largest, publicly listed, most representative, and domestically domiciled companies in both the manufacturing and services sectors. The Y-axis is percentage growth.

Fig 4. Equity Price analysis of 5 of the most representative, domestically-domiciled Manufacturing firms in India demonstrate varying, dispered growth trends. Source: LSEG Workspace

Fig 5. Equity Price analysis of 5 of the most representative, domestically-domiciled Service firms in India indicate across-the-board growth. Source: LSEG Workspace

While top-performing firms in the manufacturing sector—notably Maruti Suzuki (+795%) and Reliance Industries (+407%)—delivered higher individual equity returns, the services sector exhibited more consistent and broad-based growth. All five services firms posted positive returns, led by Bharti Airtel (+482%) and IndiGo (+364%), with even PSU (Public Sector Undertaking/State-Owned Enterprises) entities like SBI (+270%) and CONCOR (+119%) in the green. In contrast, manufacturing displayed greater dispersion, with strong gains offset by a prolonged decline in BHEL (−36%) and weak growth in Tata Steel (+124%). A preliminary observation suggests that while manufacturing offered selective upside, services provided a more reliable and sector-wide equity uplift over the 2014–2025 period. More tellingly, Reliance Industries’ exceptional performance can be attributed to the strategic evolution of its business model. Originally a petrochemicals and refining giant, the company made a bold foray into telecommunications in 2016 with the launch of Jio, which rapidly became India’s largest telecom provider. This pivot marked a fundamental shift in Reliance’s corporate DNA—from a pure-play industrial enterprise to a manufacturing-backed, consumer-facing conglomerate. By leveraging its industrial cash flows to build scalable digital and retail platforms, Reliance repositioned itself closer to the end consumer, significantly enhancing its market valuation.

Therefore, it seems that Indian economy rewarded manufacturing firms that aligned with a consumption-driven, platform-led services model. Manufacturing that remained capital-heavy and are situated upstream in the supply chain struggled (BHEL, Tata Steel) — while those that hybridized or rode consumption tailwinds (Reliance, Maruti) soared.

Lastly, we can understand the sub-par performance of the initiative by looking at employment growth in the manufacturing sector.

Figure 6. Employment Figures for Manufacturing shows sub-par growth. Source: ASI, MoSPI

A modest 3.64% CAGR in manufacturing employment aligns closely with the 2.7% CAGR in manufacturing output recorded between 2014 and 2023. The former is largely contingent on the latter: when output growth remains sluggish, firms face little incentive to expand capacity or hire additional labor, resulting in subdued employment growth. An apt insight, therefore, is this: while India has seen isolated gains in higher-margin manufacturing, overall output has been stagnant and even declining both in absolute and relative terms. Outliers exist, but the general trajectory falls short of expectations. The “Make in India” therefore seems to not be effective in achieving the initial objectives that the government set out to do. Its initial desire to become the next manufacturing powerhouse in Asia seems to be an overdue promise that it failed to deliver.